The World is Watching Tankers. It Should be Watching Supply Chains.

Even if the Strait of Hormuz reopened tomorrow, the real disruption would still be ahead of us. The markets have moved on the headline but supply chains do not. They absorb a shock, hold it for a while, then pass it on, through inventories, refineries, freight networks and supplier tiers most organisations struggle to see.

In short

- The visible shock is happening at sea. The more damaging one is still moving through the system.

- Reopening Hormuz would not restore normality overnight. Shipping, insurance and port operations would take months to rebalance.

- The pressure will show up in products - petrochemicals, diesel and jet fuel - before many buyers fully connect it to upstream energy flows.

- Inventories and cargoes already in transit bought the system time. That buffer is thinning.

- The companies most exposed are often not the ones with weak tier-one suppliers, but the ones with poor visibility beyond them.

The lag is the story

Six weeks into the Gulf crisis, the debate has narrowed to a familiar question: is the Strait of Hormuz open, closed, or somewhere in between? Markets have swung with every change in that story. But it is the wrong place to stop. The biggest consequences for supply chains do not land when the headline breaks, they arrive later, when the physical system starts to catch up.

A shock still working through the system

The headline numbers are stark. Around 13 million barrels per day of oil production and 2.7 million barrels per day of refining capacity remain offline. Cumulative supply losses have already exceeded 550 million barrels. Tanker transits through Hormuz have fallen by roughly 90%.

But scale is only half the story it is the timing that matters more.

A cargo that fails to leave today does not become a problem today. It becomes a problem weeks later, when the vessel should have docked, when inventories should have been drawn down, when production plans should have turned into output.

As the World Bank has noted, supply chain disruptions propagate with delay, often surfacing in production and pricing weeks or months after the initial shock. That lag is where the real damage sits.

Six weeks into the disruption, shipping activity has not meaningfully rebounded. Tanker movements through the Strait of Hormuz remain down by roughly ninety percent compared with normal levels. While there have been isolated departures, these have not translated into a sustained increase in flows, indicating that the physical routing of oil remains severely constrained.

Reopening is not recovery

There is still an assumption that once the strait reopens, normal service will follow. But analysis points the other way. Even in a relatively optimistic scenario, flows stay subdued through April, recover only partially from May to July, and do not settle into a new steady state until October.

That should not surprise anyone who has run an operation. Shipping networks have to rebalance. Vessels have to be repositioned. Insurance has to be repriced. Ports have to work through congestion. Recovery doesn’t happen immediately; it is a sequence.

The International Maritime Organization has consistently highlighted that disruptions to global shipping networks can take months to normalise, as vessel displacement, port congestion and contractual adjustments work their way through the system.

Traffic through the Strait is expected to remain below average until April with only a partial improvement anticipated in the middle of the year. This indicates that the disruption persists at the present stage. Activity is described as recovering 70% of the initial decline during May to July before gradually returning to a new steady level by October period. This overall framing emphasises a slow and uneven normalisation rather than a rapid return to prior conditions.

Why this goes well beyond oil

Hormuz is not a marginal route. The U.S. EIA describes it as the world’s most important oil chokepoint. In 2024 and early 2025, more than one-quarter of global seaborne oil trade moved through it. Around one-fifth of global oil and petroleum product consumption depended on it. Around one-fifth of global oil and petroleum product consumption depended on it. And 84% of the crude and condensate moving through the strait went to Asian markets, with China, India, Japan and South Korea the most exposed.

That matters more than it first appears. State of Flux research shows that more than 50% of an organisation’s workforce and over 50% of its end-customer experience are delivered through suppliers. When energy flows tighten, the impact does not stay upstream. It moves quickly into the extended enterprise.

Follow the products, not the barrels

Start with Propane and naphtha. Propane is a petrochemical feedstock used to make olefins, which then become plastics, resins, solvents, coatings and adhesives. Naphtha is another critical feedstock used in crackers to produce the building blocks of plastics. When those flows tighten, the effect does not stop at energy. It moves into packaging, automotive components, consumer goods, industrial materials, paints, films, medical supplies and the countless intermediate products buried inside larger assemblies.

Then take diesel, this fuel underpin trucks, locomotives, agricultural equipment, industrial machinery, heating and some power generation. Put simply, diesel keeps goods moving, crops harvested, sites operating and logistics intact. When diesel tightens or spikes in price, the pressure does not stay neatly inside a fuel budget. It spreads into freight, warehousing, inbound materials, food production, field service, construction, maintenance and last-mile delivery.

Jet fuel matters just as much. IATA notes that aviation fuel is one of the largest airline operating costs and that a reliable supply chain from refinery to wingtip is critical. Reuters has reported that even where outright shortages have not yet materialised, authorities and airlines remain concerned, and industry leaders have warned that jet fuel supply could take months rather than weeks to recover fully. That means pressure on air freight, passenger capacity, lead times, premium transport costs and high-value, time-sensitive supply chains.

The downstream impact is already visible in pricing. Recent Morgan Stanley research shows that while refined products such as diesel, jet fuel, and key petrochemical feedstocks have eased from recent peaks, prices remain well above pre-conflict levels. This suggests that stress in product markets is persisting even as the most visible market signals appear to stabilise.

The buffer is running out

At the outset of the crisis, the system still had some resilience. Inventories and cargoes already in transit provided a temporary cushion.

That cushion is thinning fast. Analysis shows a sharp decline in oil-on-water, alongside tightening inventories and delayed cargo arrivals following earlier export declines.

This is the point at which the system stops absorbing disruption and starts passing it on.

Crude oil volumes in transit are declining rapidly, with the most significant decline observed in cargoes destined for Northeast Asia. The overall level of oil moving between regions is being drawn down, signaling that existing in-transit supply is diminishing rather than holding steadily.

Cargo arrivals are easing only after an earlier decline in departures, reflecting a clear lag between outbound and inbound movements. This delayed adjustment suggests that previously available buffers are now being worked through, resulting in current arrival levels weaker or lower than what prior shipping activity had indicated.

Where the real exposure sits

This is why the major disruption is still to come. The first shock is visible in prices and vessel-tracking data. The second arrives later, inside production schedules, service levels and working capital. The third arrives later still, when buyers realise they do not just have a supplier problem. They have a tier-two, tier-three and tier-four visibility problem.

Too many organisations still manage suppliers as though risk ends at the first contract boundary. It does not. If your supplier relies on a converter, which relies on a chemicals producer, which relies on petrochemical feedstock, which in turn relies on constrained energy and shipping routes, then your exposure sits several steps upstream from where your procurement system stops.

The companies that will struggle most are not necessarily the ones with the weakest direct suppliers. More often, they are the ones with the weakest line of sight beyond them.

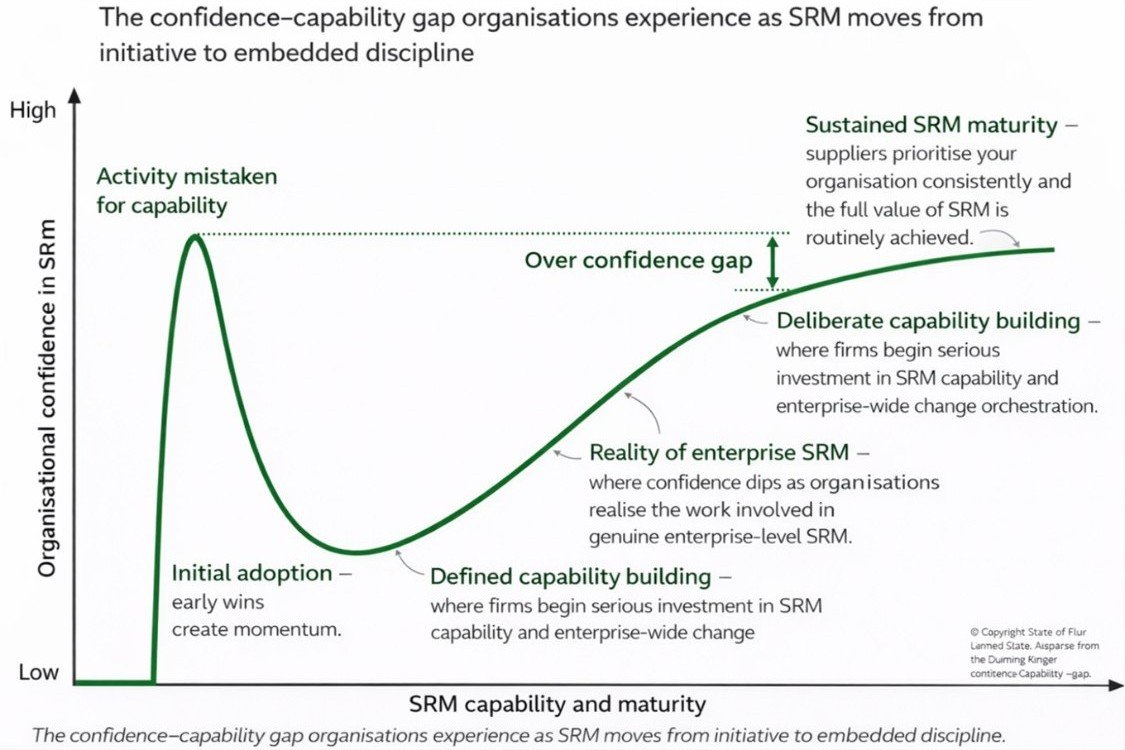

Busy is not the same as prepared

In moments like this, organisations usually accelerate. More meetings. More dashboards. More reporting.

That can create a dangerous illusion of control.

The Dunning-Kruger capability curve helps explain why. Early activity builds confidence long before real capability is in place. In supplier management, that often shows up as organisations assuming they are mature because they are busy.

State of Flux global SRM research consistently shows a gap between perceived and actual capability. Organisations that rate themselves highly often lack the global governance, segmentation discipline and supplier engagement required to perform under stress.

But maturity is not measured in motion. It is measured in outcomes: speed of decision-making, clarity of escalation, depth of supplier engagement, and the ability to act across the enterprise.

Why SRM will decide who copes best

In stable conditions, contracts govern. In unstable conditions, relationships decide.

When supply is constrained, suppliers allocate scarce capacity. Those decisions are shaped by accumulated experience. Contracts provide rights. Relationships influence behaviour.

State of Flux research shows that only around 9% of organisations are recognised by suppliers as a “Customer of Choice.” Those organisations are significantly more likely to receive early warning, preferential allocation and collaborative problem-solving during disruption.

In a constrained system, those advantages compound. Organisations that are trusted are more likely to receive capacity, attention and transparency. Those that are not will find that contractual leverage offers only limited protection.

The question boards should be asking

For boards and executive teams, the real question is not when the Strait of Hormuz reopens. It is whether the organisation is ready for what follows.

Three actions matter now.

See beyond tier one. Map critical dependencies across supplier tiers, especially where energy and petrochemical inputs sit upstream. Then re-run your supplier segmentation so you understand where supplier risk really sits. We recommend identifying which products and services carry the greatest customer and profit impact, and making that one of the key criteria in the segmentation.

Engage key suppliers properly. Do not simply ask for updates. Use the moment to understand constraints, align priorities and co-develop response plans. Make sure your people know how to do this well, and that the business is speaking with one voice to those suppliers.

Treat SRM as enterprise infrastructure. Supplier Relationship Management is not just a procurement process. It is a cross-business capability that connects commercial intent, operational delivery and executive behaviour.

The companies that act now will not avoid disruption. But they will move through it with greater clarity, speed and control. The rest will discover, too late, that the real disruption was never only in the strait. It was in the system that depended on it.

Make supplier segmentation work in practice

Most organisations segment suppliers. Fewer use it to guide decisions. When segmentation reflects real business impact, it becomes a way to prioritise effort, align stakeholders, and focus attention where it matters. See how supplier segmentation is applied within a broader supplier management approach.